It explains the connection between a company’s income statement and balance sheet. Mainly, there are three sections of this statement that include the following. Web this module focuses on the requirements for presenting changes in an entity’s equity for a period applying section 6 statement of changes in equity and statement of income and retained earnings of the ifrs for smes standard. Find a statement of changes in equity example. Web the statement of changes in stockholders’ equity should distinguish equity attributable to the parent from equity attributable to noncontrolling interests.

Web the statement of changes in equity is one of the main financial statements. It reconciles the opening balances of equity accounts with their closing balances. Web statement of stockholder’s equity, often called the statement of changes in equity, is one of four general purpose financial statements and is the second financial statement prepared in the accounting cycle. Web to get a solid understanding of a statement of changes in equity we’ll explore what is included in this statement, how it’s structured, and how to interpret its valuable insights, accompanied by practical examples. Find a statement of changes in equity example.

Web statement of changes in equity (all you need to know) this statement helps to understand the wealth of the company owner and how it has changed in the years under consideration. Web statement of stockholder’s equity, often called the statement of changes in equity, is one of four general purpose financial statements and is the second financial statement prepared in the accounting cycle. This statement displays how equity changes from the beginning of an accounting period to the end. A reconciliation between the carrying amount at the beginning and the end of the period of each component of equity, such as share capital, retained earnings, and revaluation. This report tracks changes in retained profits, other reserves, and share capital, such as issuing new shares and the payment of.

PPT Lesson 2 Rules of Accounting and Financial Reports PowerPoint

3.5 Statement of Changes in Equity (IFRS) and Statement of Retained

Statement Of Stockholders Equity Template

Statement Of Changes In Owner's Equity Excel Template And Google Sheets

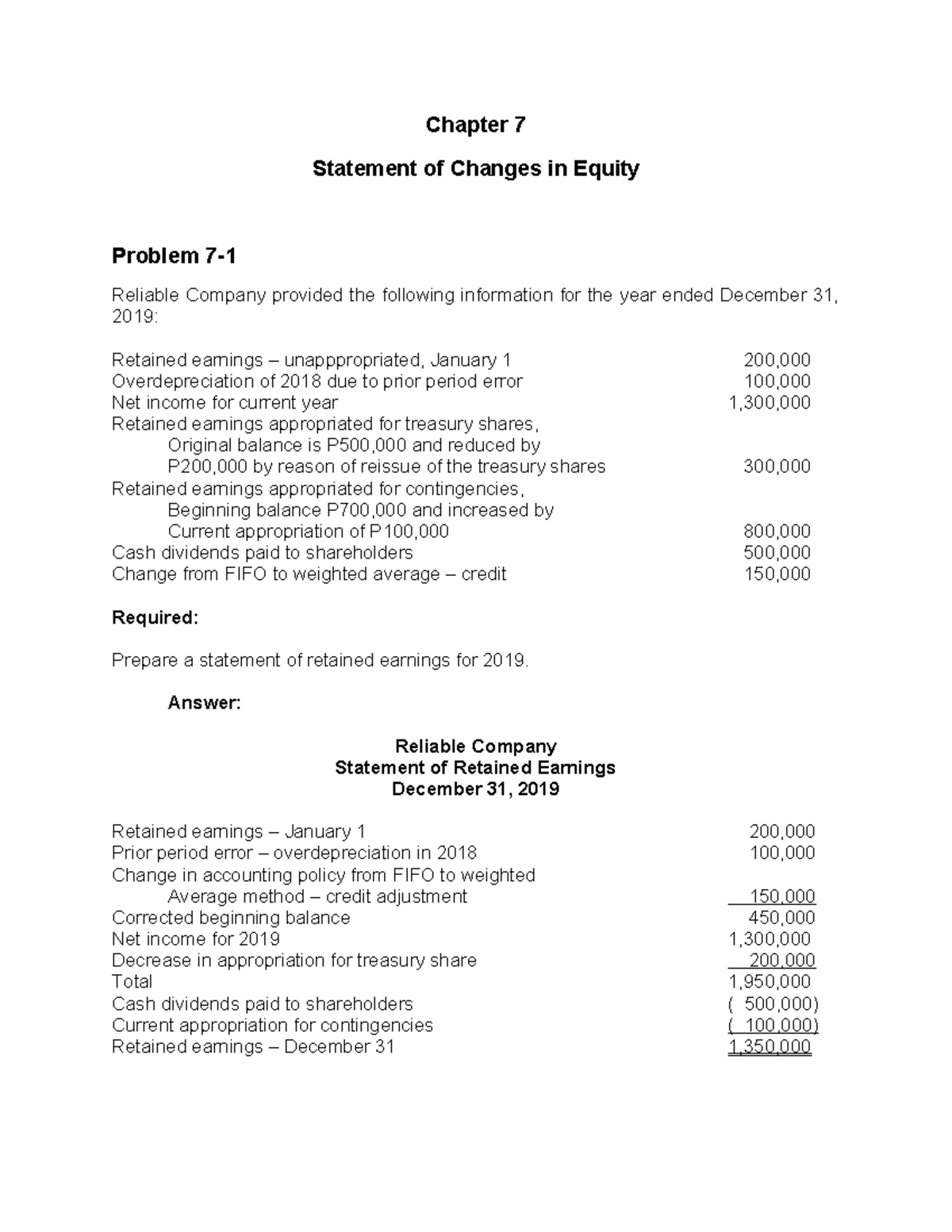

Statement of changes in equity required 3 pdf free Chapter 7

Statement of Change in Equity Financial Report Template Venngage

Statement of Changes in Equity YouTube

EXCEL of Statement of Changes in Equity.xls WPS Free Templates

Simple Statement of Change in Equity Financial Report Template Venngage

PPT Corporate Finance A1 PowerPoint Presentation, free download ID

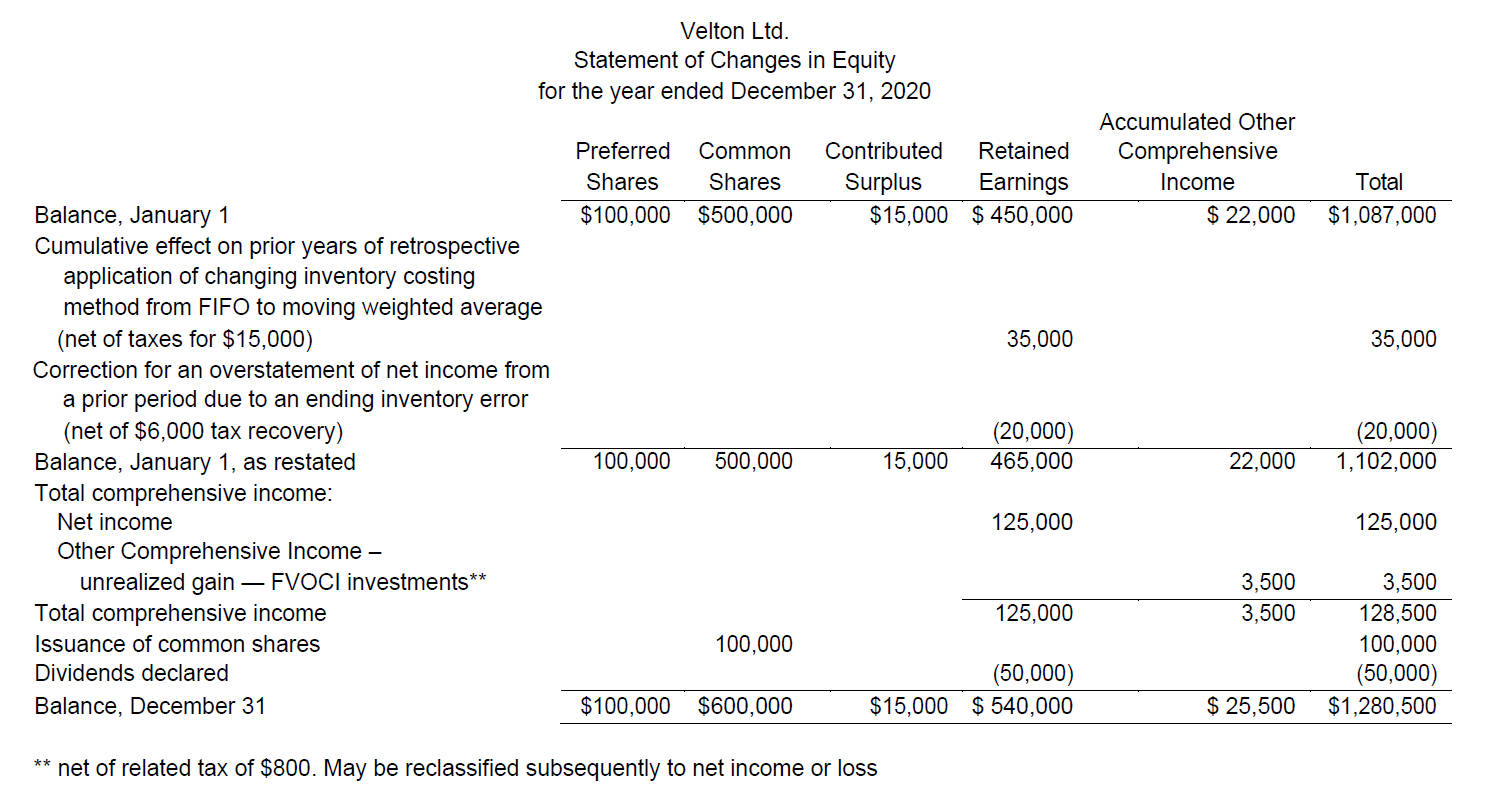

Web this module focuses on the requirements for presenting changes in an entity’s equity for a period applying section 6 statement of changes in equity and statement of income and retained earnings of the ifrs for smes standard. The purpose of the statement is to show the equity movements during the accounting period and to reconcile the beginning and ending equity balances. Web 6.3 statement of changes in equity. It explains the connection between a company’s income statement and balance sheet. This report tracks changes in retained profits, other reserves, and share capital, such as issuing new shares and the payment of. The following is an example of the statement of changes in equity for an ifrs company, velton ltd.,. It reconciles the opening balances of equity accounts with their closing balances. A reconciliation between the carrying amount at the beginning and the end of the period of each component of equity, such as share capital, retained earnings, and revaluation. A statement of change in equity is a financial statement that shows the changes in the share owner’s equity over a specific accounting period. Web learn about a statement of changes in equity and the closely related statement of changes in owner's equity. Web the statement of owner’s equity reports the changes in company equity, from an opening balance to and end of period balance. Web the statement of changes in equity is one of the main financial statements. Mainly, there are three sections of this statement that include the following. Web for ifrs companies, each account from the equity section of the sfp is to be reported in the statement of changes in equity. Web the statement of changes in equity is a reconciliation of the beginning and ending balances in a company’s equity during a reporting period.

It Reconciles The Opening Balances Of Equity Accounts With Their Closing Balances.

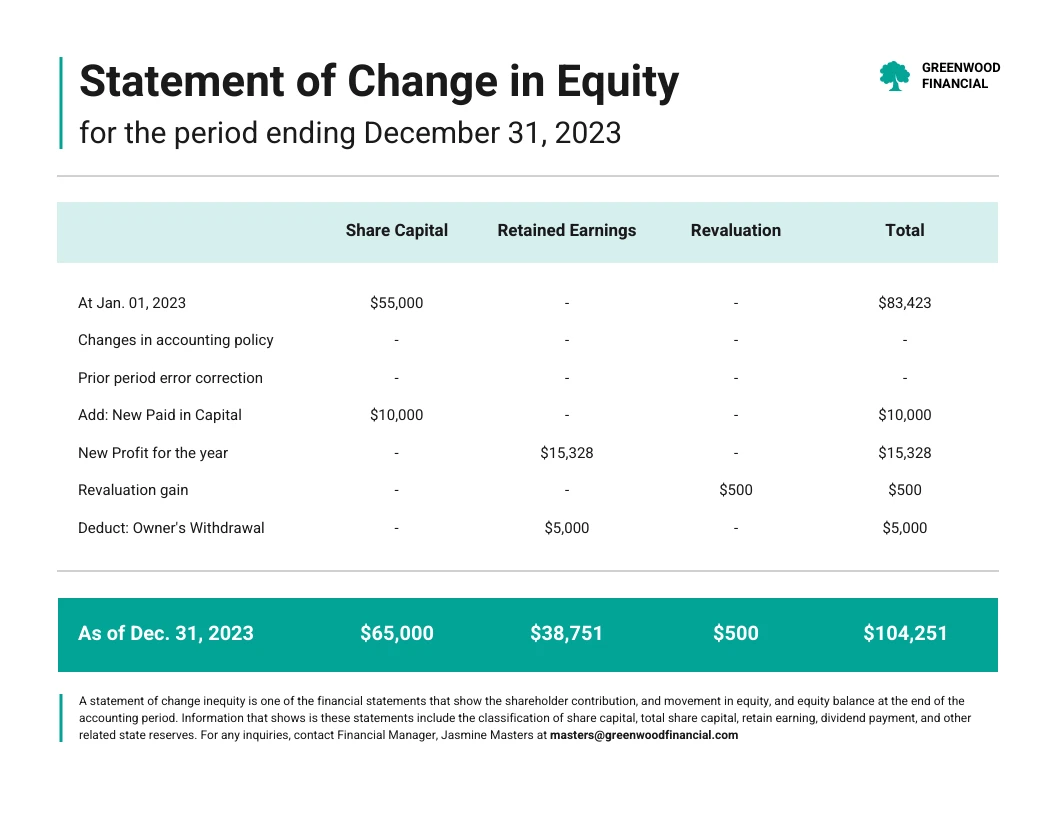

Web the statement of changes in equity is a reconciliation of the beginning and ending balances in a company’s equity during a reporting period. It reconciles the opening balances of equity accounts with their closing balances. Edit it with a monochromatic color scheme, a classic font, and bold headings. Share capital, contributed surplus, accumulated other comprehensive income, and retained earnings.

Check Out Venngage For More Minimal Report Templates.

Web this module focuses on the requirements for presenting changes in an entity’s equity for a period applying section 6 statement of changes in equity and statement of income and retained earnings of the ifrs for smes standard. Web learn about a statement of changes in equity and the closely related statement of changes in owner's equity. Web statement of change in equity template for excel. Web the statement of changes in stockholders’ equity should distinguish equity attributable to the parent from equity attributable to noncontrolling interests.

This Statement Displays How Equity Changes From The Beginning Of An Accounting Period To The End.

The purpose of the statement is to show the equity movements during the accounting period and to reconcile the beginning and ending equity balances. Web statement of stockholder’s equity, often called the statement of changes in equity, is one of four general purpose financial statements and is the second financial statement prepared in the accounting cycle. The purpose of this statement is to convey any change (or changes) in the value of shareholder’s equity in a company during a year. Web ifrs requires a statement of changes in equity to be presented as a primary statement for all entities.

The Changes Include The Earned Profits, Dividends, Inflow Of Equity, Withdrawal Of Equity, Net Loss, And So On.

Web to get a solid understanding of a statement of changes in equity we’ll explore what is included in this statement, how it’s structured, and how to interpret its valuable insights, accompanied by practical examples. It is a financial statement that summarizes the transactions affecting the shareholder’s equity during a specific period. Web for ifrs companies, each account from the equity section of the sfp is to be reported in the statement of changes in equity. Web the statement of owner’s equity reports the changes in company equity, from an opening balance to and end of period balance.